Lacking Virtu?

An Asset - Liability Mismatch?

“Fewer possess virtue, than those who wish us to believe that they possess it.” - Cicero

The Epstein files documented his involvement in naked shorting and market abuse. This has made the claims of whistleblower Chris J. Dilorio, detailed in 50 pages of these files, all the more poignant. The various emails from Dilorio alleging massive Wall St. fraud are linked here:

I wrote about those claims in my last Substack piece entitled “The Epstein Files And Naked Shorting” which is linked below. Given these revelations I thought I’d dig deeper in into the allegations. Dilorio writes harshly about many involved in the trading of securities, from individuals to regulatory agencies to several financial firms. Of the latter, his biggest criticism is of Virtu Financial which uses VIRT and NITE as it’s identifier for market making. The NITE is from its 2017 takeover of the failed Knight Securities. Virtu derives the majority of its income from market making. It makes markets in over 25,000 securities in 37 different countries and on over 200 different trading venues. It is one of the leading market makers on the OTCM market which is where many small and microcap companies trade. Following are some excerpts from Dilorios emails:

6/23/20

The core business at NITE (Virtu) is and always has been: abusive naked shorting OTCM shells to facilitate money laundering.

2/17/2021

“This is NOTHING and I mean NOTHING compared to the naked shorting going on in the OTCM and clearly evident on the NITE/VIRT balance sheet.”

The Core business at Knight/KCG/VIRT:NITE is and ALWAYS has been abusive naked shorting OTCM (and other) Money laundering shells to facilitate money laundering. ACTIVELY facilitated by the grossly corrupt SEC scumbags for the benefit of the criminals like NITE/VIRT,CDEL who OWN them.

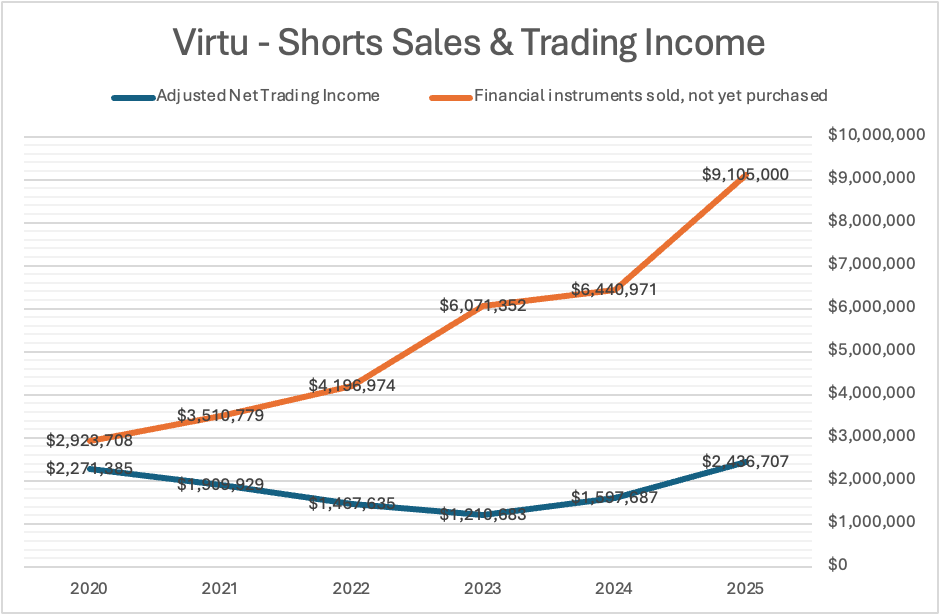

Given these accusations it is worth looking at Virtu’s financial data per its 10-K’s and other earnings releases to see if there is any evidence of the allegations. For those of you unfamiliar with SEC Regulations, under Reg SHO, a market maker is allowed to sell securities it does not own and has not borrowed in order to keep an “orderly market”. If the shares are not borrowed first before being sold, which they are not when sold using Reg SHO, then they are naked shorts. These naked shorts are supposed to be covered within 5 trading days. It is Dilorio’s contention that Virtu abuses Reg SHO and that many of these shares are never bought back. If so, this should show up on the balance sheets of Virtu. Starting with 2020 we examined Virtu’s financial filings through to 2025. The first thing that stuck out like a sore thumb was the explosive growth of “Financial Instruments Sold, Not Yet Purchase” as the chart below shows:

These grew by over $6 billion during the period. That is 311% total growth, or an annualized increase of 32.7% in naked shorts! Now if this was due to a boom in trading it would be explainable. But as the chart above shows this is not the case as total trading income over the period rose only 7.3%.

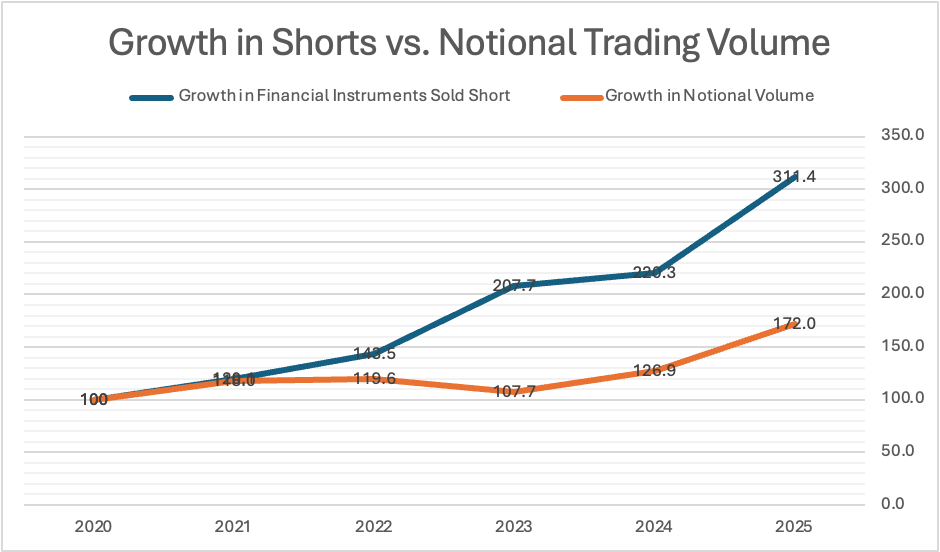

Another means is by comparing the growth in naked shorting with notional $ trading value. The chart below shows a similar pattern (rebased to 100):

As stated above naked shorts grew 311% against a 72% growth (the majority of which occurred in 2025) in notional $ trading value. Virtu grew its naked short book at a rate far exceeding both trading volume and income.

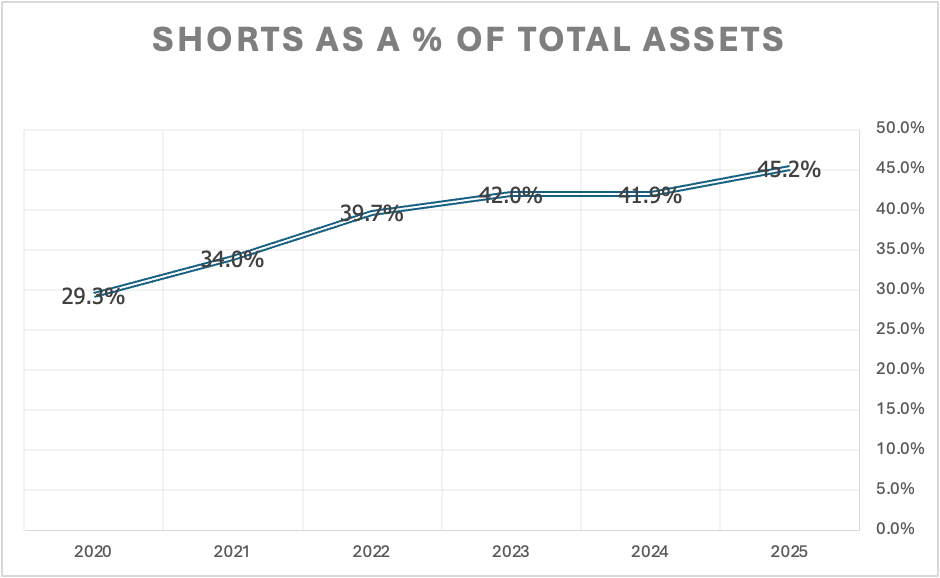

As short sales are a liability, the offsetting asset is financial assets owned outright. When Virtu sales a security short it purchases assets or increases cash. The rate of cash increase has been meager only growing by about $200 million between 2020 and 2025. The securities purchased with the proceeds of the short sales are not disclosed on the balance sheet. As the chart below shows, shorts have become an increasing part of the balance sheet and now account for 45.2% of total assets, up from 29.4% in 2020.

This is the biggest issue with the balance sheet of Virtu. There is zero transparency on what constitutes the $9 billion of naked shorts on its book. There is also no transparency on the makeup of the offsetting financial assets that it owns. According to Dilorio, most of the shorts are stocks which trade on the OTCM market. The vast majority of these stocks have no options or other derivatives which would allow Virtu to hedge these positions. If one of these companies has a GameStop like surge one has to wonder if Virtu would survive.

Is this explosion in the short position and the need to defend it, why Virtu has been accused of engaging in abusive market practices? It is currently a defendant in three court cases alleging market abuse:

Asia Broadband, Inc. v. Virtu Financial Inc., et al. (U.S. District Court for the Central District of California). Virtu is being sued for allegedly engaging in securities fraud and coordinated market manipulation over an extended period.

Genius Group Limited v. Citadel Securities LLC and Virtu Americas LLC (S.D.N.Y.): Genius alleges spoofing and naked short selling of GNS stock.

Northwest Biotherapeutics, Inc. (NWBO) v. Canaccord Genuity LLC, et al. (including Virtu Americas; S.D.N.Y.): NWBO is suing for spoofing and market manipulation.

Then there are these cases which allege various management malfeasances:

Iron Workers Local No. 55 Pension Fund v. Virtu Financial, Inc. (Delaware Chancery): Ongoing shareholder fiduciary/class action over alleged self-dealing via buybacks and control structure (~$400M diversion claim).

In re Virtu Financial, Inc. Securities Litigation (E.D.N.Y., consolidated class action): Ongoing securities fraud class action (class period ~2018/2019–2023) alleging misleading statements about information barriers; class certification motion briefed as of late 2025.

The former case is of note and per Grok:

Allegations:

Founder/controlling stockholder Vincent Viola (via affiliates like TJMT Holdings LLC), ex-CEO Douglas Cifu, and other insiders allegedly breached fiduciary duties by exploiting Virtu’s dual-class/two-tiered corporate structure.

Through massive share repurchase programs (buybacks), insiders purportedly diverted ~$400 million from public Class A stockholders to themselves, families, and associates.

The scheme allegedly relies on disproportionate benefits to controlling interests (e.g., via LLC unit mechanics, voting control, and exchanges) at the expense of ordinary shareholders, constituting self-dealing and ongoing harm.

Are these buybacks evidence of the money laundering? Recycling illicit gains through dividend pay outs would be a clever way to do so. Perhaps, this case will shed some light on the matter.

Thinking about it, the whole situation is insane. Virtu is a company that appears to have blatantly abused the market maker exception to shorting and has tripled its naked short position over the last five years. This was done at a rate far outstripping growth in underlying trading revenue or volume.

Naked shorting has a pernicious effect on companies as it creates false markets for their securities and drives up their cost of capital. As a shareholder of NWBO I have first hand experience with the toll naked shorting takes.

This state of affairs proves Cicero right. Despite its name there is little virtue at Virtu.

Or you could

My previous article on the Epstein Files:

The author is a shareholder of NWBO. I am not a financial adviser. This is not financial advice or a recommendation to buy or sell NWBO stock and should not be interpreted as such. I have not received compensation of any type from the company or any related party for this article.